As you approach retirement age or consider your property ownership decisions in Singapore, understanding the Central Provident Fund (CPF) retirement sums becomes crucial for your financial planning. The CPF retirement sums—comprising the Basic Retirement Sum (BRS), Full Retirement Sum (FRS), and Enhanced Retirement Sum (ERS)—serve as reference points to help determine how much you need to save for your desired monthly payouts during retirement.

What Are CPF Retirement Sums?

CPF retirement sums are reference amounts that provide guidance on how much savings you require in your CPF accounts to achieve specific monthly payout levels during retirement. These amounts are determined when you turn 55 years old and remain fixed for the rest of your life, serving as the foundation for your retirement income through the CPF LIFE scheme.

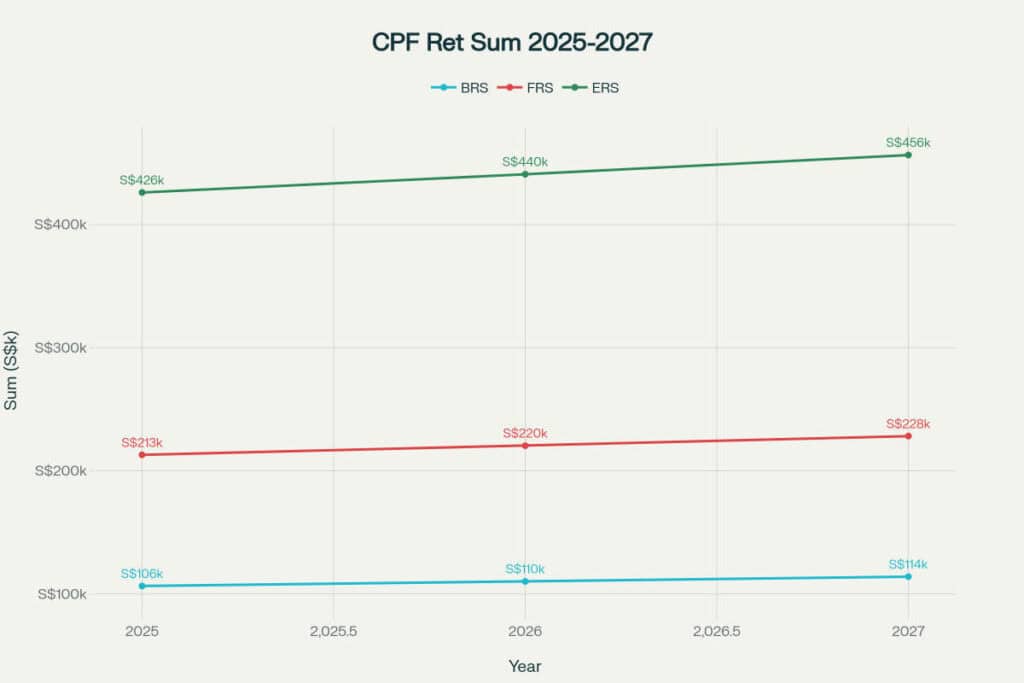

The chart above illustrates how CPF retirement sums have been structured to increase annually from 2025 to 2027, accounting for inflation, longer life expectancy, and improvements in standard of living.

Basic Retirement Sum (BRS): Your Foundation for Retirement

What is the Basic Retirement Sum?

The basic retirement sum provides monthly payouts designed to cover basic living needs during retirement, excluding rental expenses. For those turning 55 in 2025, the BRS is set at S$106,500. This amount is based on expenditure from a lower-middle retiree household, according to the latest Household Expenditure Survey, and assumes that you own a property lasting until age 95.

The BRS takes into account that property owners will not need to worry about rental costs during retirement, making it suitable for those who have secured their housing needs.

Key Features of BRS

- Fixed for Life: Once set when you turn 55, your BRS remains constant throughout retirement.

- Property Consideration: Designed for property owners who will not have rental expenses.

- Automatic Qualification: About 8 in 10 active CPF members turning 55 in 2027 are expected to meet the BRS, representing the highest attainment rate among all cohorts.

Full Retirement Sum (FRS): The Ideal Reference Point

Understanding the Full Retirement Sum

The full retirement sum represents an ideal reference point for retirement savings, set at exactly two times the BRS. For those turning 55 in 2025, the FRS amounts to S$213,000. This sum is designed to provide higher monthly payouts that can cover both living expenses and rental costs for those who do not own property.

Important FRS Rules

When you turn 55, your Special Account (SA) savings will be transferred first to your newly created Retirement Account (RA) to meet the FRS, followed by your Ordinary Account (OA) savings if needed. If you have savings exceeding the FRS, you can withdraw the excess amount in cash, subject to certain conditions.

Property Owners’ Advantage: If you own a property with a remaining lease lasting until at least age 95, you can set aside your FRS using a mixture of property pledge (up to half the FRS, which equals the BRS) and cash. This flexibility allows you to withdraw RA savings down to the BRS level.

It is worth noting that while this provides short-term liquidity, it reduces the guaranteed monthly income available in retirement.

Enhanced Retirement Sum (ERS): Maximum Retirement Security

What is the Enhanced Retirement Sum?

The enhanced retirement sum represents the maximum amount you can set aside in your Retirement Account for the highest possible monthly payouts. Starting from 2025, the ERS has been raised to four times the BRS, amounting to S$426,000. This increase from the previous three times multiplier reflects the government’s commitment to providing higher retirement income options.

Key ERS Changes in 2025

- Increased Multiplier: The ERS rose from 3× BRS to 4× BRS in 2025.

- Current Year Basis: Unlike BRS and FRS, which are fixed when you turn 55, the ERS follows the current year’s amount regardless of when you turned 55.

- Voluntary Nature: You can choose to top up to the ERS anytime from age 55 onwards for higher retirement payouts.

Monthly Payout Comparisons

The chart above demonstrates the significant differences in monthly payouts based on your chosen retirement sum level. For members turning 55 in 2025 under the CPF LIFE Standard Plan:

| Retirement Sum Level | Amount Required at 55 | Estimated Monthly Payout from Age 65 |

|---|---|---|

| Basic Retirement Sum | S$106,500 | S$860 – S$930 |

| Full Retirement Sum | S$213,000 | S$1,610 – S$1,730 |

| Enhanced Retirement Sum | S$426,000 | S$3,100 – S$3,330 |

Property Pledge Options: Maximising Your Flexibility

Eligibility Requirements for Property Pledge

Property owners have unique advantages when managing their CPF retirement sums. To utilise property pledging options, you must meet specific criteria:

- Age Requirement: You must be 55 years old or above.

- Property Ownership: You must own a completed property in Singapore.

- Lease Duration: The remaining lease must last until you are at least 95 years old.

- Adequate Refund Capacity: The expected CPF housing refund must be sufficient to restore withdrawn amounts when you sell the property.

How Property Pledge Works

- For Properties Purchased with CPF: You can withdraw RA savings as long as your remaining retirement sum after withdrawal, plus the CPF savings used for the property (including accrued interest), equals your FRS.

- For Properties with Minimal CPF Usage: You can still withdraw RA savings by pledging to refund the withdrawn amount when you sell or transfer the property, subject to valuation and loan assessments.

Example: Property Owner’s Strategy

Consider Mr Lim, who turns 55 in 2025:

- Without property pledge: Must set aside the full FRS of S$213,000 in his RA.

- With property pledge: Can set aside only the BRS of S$106,500 in cash and withdraw up to S$106,500 from his RA for immediate needs, using his property to make up the remaining FRS portion.

This strategy provides immediate liquidity while maintaining retirement security, though it results in lower monthly payouts during retirement.

Recent FRS Updates and Changes

2025 Key Changes

Several significant updates took effect in 2025 that directly impact retirement planning:

- Special Account Closure: The CPF Special Account closes when members reach 55, with balances transferred to the Retirement Account up to the FRS limit.

- Enhanced Retirement Sum Increase: The ERS multiplier increased from 3× to 4× the BRS, providing greater savings potential.

- Contribution Rate Changes: CPF contribution rates for senior workers aged 55–65 increased by 1.5%, with employers contributing an additional 0.5% and employees contributing 1% more.

Future Projections

The government has announced retirement sums through 2027 to help members plan ahead:

| Year Turning 55 | BRS | FRS | ERS |

|---|---|---|---|

| 2025 | S$106,500 | S$213,000 | S$426,000 |

| 2026 | S$110,200 | S$220,400 | S$440,800 |

| 2027 | S$114,100 | S$228,200 | S$456,400 |

These increases of about 3.5% annually account for inflation and rising living standards.

One implication is that younger cohorts will need to plan for higher savings levels compared with today’s retirees.

Practical Strategies for Soon-to-Retire Individuals

Voluntary Top-Up Considerations

- Tax Relief Benefits: You can enjoy tax relief of up to S$8,000 annually for cash top-ups to your own CPF accounts, plus an additional S$8,000 for top-ups to family members’ accounts, according to CPF Relief for Employees.

- Interest Earnings: CPF accounts offer attractive interest rates of up to 6% per annum for those 55 and above, with additional interest on the first S$60,000 of combined balances.

- Strategic Timing: Consider making voluntary top-ups before age 55 to your Special Account, or after 55 to your Retirement Account, depending on your goals.

Property Owners’ Decision Framework

When deciding whether to pledge your property, consider these factors:

Advantages:

- Immediate access to cash (up to BRS amount).

- Maintain property ownership.

- Flexibility for other investments or expenses.

Disadvantages:

- Lower monthly retirement payouts.

- Obligation to refund withdrawn amounts upon property sale.

- Reduced sales proceeds when selling property.

Maximising Your Retirement Income

CPF LIFE Plan Selection

Understanding your options within CPF LIFE can help optimise your retirement strategy:

- Standard Plan: Provides steady monthly payouts, suitable for most retirees seeking consistent income.

- Basic Plan: Offers lower initial payouts but preserves more funds for beneficiaries.

- Escalating Plan: Starts with lower payouts that increase by 2% annually, providing inflation protection.

Long-Term Planning Tips

- Start Early: The power of compound interest makes early contributions significantly more valuable.

- Regular Reviews: Monitor your retirement sum projections using CPF calculators.

- Holistic Approach: Consider CPF retirement sums as part of your broader retirement portfolio, including other investments and insurance coverage.

Conclusion and Action Steps

Understanding CPF retirement sums is essential for making informed decisions about your retirement and property ownership. The BRS provides basic coverage for property owners, the FRS offers comprehensive retirement security, and the ERS delivers maximum monthly income for those seeking premium retirement lifestyles.

Key Takeaways:

- Your retirement sums are fixed when you turn 55 and determine your lifetime monthly payouts.

- Property owners have valuable flexibility through pledge options, though this reduces retirement income.

- Voluntary top-ups offer tax benefits and guaranteed returns, making them attractive for boosting retirement savings.

- The 2025 changes, including the increased ERS multiplier and SA closure, create new opportunities and considerations for retirement planning.

Recommended Actions:

- Calculate Your Projections: Use CPF’s online calculators to estimate your retirement sums and monthly payouts.

- Review Property Strategy: If you own property, evaluate whether pledging aligns with your retirement income needs.

- Consider Voluntary Top-Ups: Assess whether additional contributions could help you reach your desired retirement sum level.

- Plan for Changes: Factor in the evolving CPF landscape when making long-term financial decisions.

By understanding these concepts and taking proactive steps, you can optimise your CPF retirement strategy to achieve financial security and peace of mind during your golden years.