Understanding CPF interest rates in 2025 and how to maximise your bonus interest

Singapore’s Central Provident Fund (CPF) is still the backbone of retirement planning in 2025. With government-backed base rates and extra bonus interest on top, understanding how your CPF interest is calculated helps you squeeze more out of every dollar you set aside. Think of it like chope-ing a hawker centre seat at lunch: a little strategy, big payoff.

Rates in 2025 remain steady and competitive. The Ordinary Account (OA) pays 2.5% per annum, while the Special, MediSave and Retirement Accounts (SA, MA, RA) pay 4% per annum. For members aged 55 and above, bonus tiers can lift effective returns to as high as 6% a year, without taking market risk.

Understanding CPF interest rates in 2025

CPF Base Interest Rates by Account Type in 2025

The CPF Board reviews interest rates quarterly to keep your returns competitive, while guaranteeing minimum floors for stability. For 2025, the structure looks like this:

Base interest rates:

- Ordinary Account (OA): 2.5% per annum

- Special Account (SA): 4.0% per annum

- MediSave Account (MA): 4.0% per annum

- Retirement Account (RA): 4.0% per annum

How interest rates are determined

The OA interest rate is pegged to the 3-month average of major local banks’ interest rates, with a legislated minimum of 2.5% per annum. That floor means your OA doesn’t dip below 2.5% even when the market turns soft.

For SA, MA, and RA, rates are tied to the 12-month average yield of the 10-year Singapore Government Securities plus 1%, with a guaranteed floor of 4% per annum currently extended until 31 December 2025.

CPF account types and their interest rates

Ordinary Account (OA)

The OA’s 2.5% rate applies to balances used for housing, education, insurance, and approved investments. While 2.5% may look modest, bonus interest on the first $60,000 of combined balances meaningfully boosts effective returns, especially when you keep at least some funds in OA to capture that sweetener.

Special, MediSave, and Retirement Accounts

SA, MA, and RA earn a higher 4% base interest because they’re meant for long-term retirement and healthcare needs. The government guarantee shields these balances from market swings, so you get reliable, compounding growth year after year.

How CPF bonus interest works

Understanding the bonus interest structure

CPF Bonus interest is designed to support all members, especially those with lower balances. Here’s the current structure:

For members below 55:

- Extra 1% CPF bonus interest on the first $60,000 of combined balances

- Up to $20,000 of that can come from OA

- Effective rates: up to 3.5% on OA and 5% on SA/MA/RA

For members 55 and above:

- Extra 2% CPF bonus interest on the first $30,000, plus

- Extra 1% on the next $30,000 of combined balances

- OA cap remains $20,000 per tier

- Effective rates: up to 4.5% on OA and 6% on SA/MA/RA

Real-world example: maximizing bonus interest

Sarah, age 35, has $80,000 across CPF ($30,000 in OA, $50,000 in SA):

- First $20,000 in OA: 3.5% (2.5% base + 1% bonus)

- Remaining $10,000 in OA: 2.5% (base)

- First $40,000 in SA: 5% (4% base + 1% bonus)

- Remaining $10,000 in SA: 4% (base)

Annual interest: ($20,000 × 3.5%) + ($10,000 × 2.5%) + ($40,000 × 5%) + ($10,000 × 4%) = $3,350

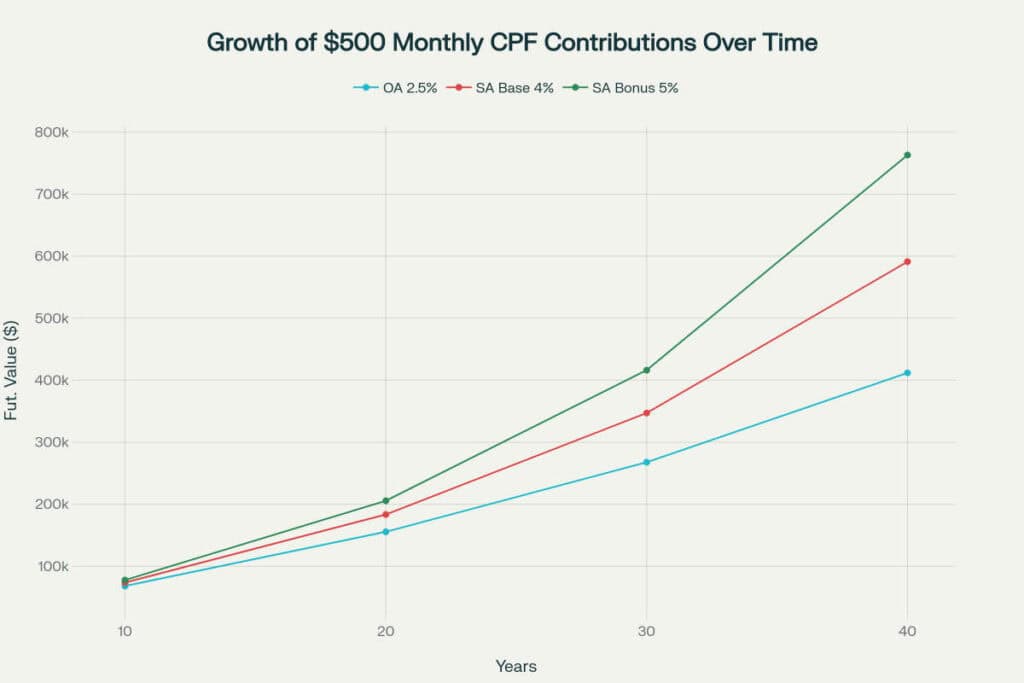

The power of compound interest in CPF

Long-term growth potential

Compound interest is where CPF quietly shines. Interest is computed monthly and credited each 1 January, which means the earlier you contribute (and the longer you leave it), the more your balance snowballs over time. This will allow you to have a higher CPF monthly payouts.

Practical examples of compound growth

Example 1: 25-year-old starting work

$50,000 initial balance over 30 years:

- OA at 2.5%: grows to $104,878 (interest: $54,878)

- OA with bonus (3.5%): grows to $119,063 (interest: $69,063)

- SA with bonus (5%): grows to $216,097 (interest: $166,097)

Example 2: 40-year-old mid-career

$100,000 balance over 15 years:

- OA at 2.5%: grows to $144,830 (interest: $44,830)

- SA mixed rates: grows to $196,773 (interest: $96,773)

Using the Rule of 72 as a quick gauge: money in SA at 4% roughly doubles every 18 years, while OA at 2.5% takes about 29 years. Slow and steady, but very real.

CPF retirement sums and monthly payouts

2025 retirement sum benchmarks

For members turning 55 in 2025:

| Retirement Sum Type | Amount at 55 | Monthly Payout at 65 |

| Basic Retirement Sum (BRS) | $106,500 | $860 – $930 |

| Full Retirement Sum (FRS) | $213,000 | $1,610 – $1,730 |

| Enhanced Retirement Sum (ERS) | $426,000 | $3,100 – $3,330 |

Enhanced Retirement Sum changes

From 2025, the ERS is four times the BRS (previously three times), letting you top up to $426,000 for higher lifelong CPF monthly payouts. Great for those who want stronger, inflation-resilient income in retirement.

CPF LIFE integration

At 55, your SA savings move into the new Retirement Account (RA), which funds CPF LIFE payouts from 65. Bonus interest still applies where eligible, helping you maximize lifetime income without extra effort.

Maximizing your CPF returns

1) Transfer from OA to SA

If housing needs are met, consider transferring excess OA to SA for the higher rate. That 1.5 percentage point gap compounds meaningfully over time.

2) Voluntary top-ups

Cash top-ups via the Retirement Sum Topping-Up (RSTU) scheme can deliver:

- Higher interest on SA/RA balances

- Tax relief up to $16,000 annually

- A faster path to the retirement sum you prefer

3) CPF Investment Scheme (CPFIS)

If you understand risk and fees, you can invest OA/SA in approved instruments. Always compare expected returns against the guaranteed CPF rates before jumping in.

CPFIS options include: unit trusts and ETFs, bonds and fixed deposits, insurance products and annuities, plus shares and REITs within limits.

Investment limits: keep $20,000 in OA and $40,000 in SA before investing, up to 35% of investible OA savings in stocks and 10% in gold.

Key changes in 2025

Special Account (SA) closure at 55

From 19 January 2025, SA closes automatically for members aged 55 and above. SA balances move to RA up to the Full Retirement Sum; any excess flows back to OA, where they still earn competitive returns.

Higher CPF contribution rates for senior workers

From 1 January 2025, total CPF contribution rates for workers above 55 to 65 increased by 1.5%, helping you build more in the crucial pre-retirement years. Hitting ERS might feel as rare as free parking in Orchard on a weekend, but these boosts do help.

Frequently asked questions

When is CPF interest credited?

It’s computed monthly and credited annually on 1 January, based on your average monthly balance for the year.

How does the bonus interest cap work?

Bonus interest applies to your combined balances up to the specified limits, with a cap on how much can come from OA. For instance, with $70,000 total ($40,000 OA, $30,000 SA), bonus interest applies to the first $60,000, but only $20,000 can be from OA.

Can I withdraw my bonus interest?

Bonus interest from OA is credited to SA or RA, growing your retirement income instead of being cashed out right away.

How are CPF savings protected?

CPF monies are invested in Special Singapore Government Securities (SSGS), guaranteed by the Singapore Government, which holds a top-tier AAA credit rating.

Key takeaways

Understanding CPF interest rates in 2025 matters for every working adult. With base rates of 2.5% (OA) and 4% (SA/MA/RA), plus up to 2% bonus interest, CPF offers competitive, risk-free growth that anchors your retirement plan.

To get the most from CPF, learn the bonus tiers, let compound interest do its job, and use smart moves like OA-to-SA transfers and RSTU top-ups. For members 55 and above, effective rates can reach 6% on selected balances, levels that many market investments struggle to match consistently over time.

For tailored strategies and projections, try CPF’s online tools or speak with a licensed adviser. The earlier you optimise your approach, the bigger the compounding tailwind that will give you a bigger CPF monthly payouts.