How Much Tax You Really Save with SRS Contributions in Singapore

- SRS cuts your taxable income: Contributing the maximum S$15,300 to the Supplementary Retirement Scheme (SRS) lowers your chargeable income, which can shrink your tax bill.

- Tax savings vary by income: Low-income earners save little to nothing (since they pay little tax to begin with), while high-income earners can save a few thousand dollars because their top income is taxed at higher rates.

- Higher income = bigger tax break: The more you earn, the higher your marginal tax rate (tax on the last dollar you earn). SRS relieves the top slice of your income, so high earners get more dollars off their tax (e.g. ~S$3k+ saved for top earners vs just a few hundred for low earners).

- Tax savings cap out: There’s a limit to the tax you can save. SRS contributions are capped at S$15,300 a year, so even millionaires can only shield that amount. In practice, the annual tax saving from maxing SRS plateaus at around S$3,000+ (because Singapore’s highest tax rate is 22%–24%).

- Long-term trade-off: SRS is meant for retirement – money is locked in until retirement age, and only 50% of withdrawals are taxable then. It’s a useful tax-deferment tool, but you should consider if locking up S$15k/year is worth a couple thousand in tax savings for your situation.

Now, let’s break down how these tax savings actually work, using Year of Assessment (YA) 2025 tax rates for Singapore residents.

SRS in a Nutshell (and How It Saves Tax)

The Supplementary Retirement Scheme (SRS) is a voluntary scheme to encourage retirement savings beyond CPF, offering tax benefits as a sweetener. When you contribute to SRS, that contribution (up to S$15,300 per year for Singapore Citizens/Permanent Residents) is deducted from your taxable income as an SRS relief. In simple terms, you don’t pay income tax on the chunk of income you put into SRS. This means a smaller portion of your income is taxed, which translates to a lower tax bill for the year.

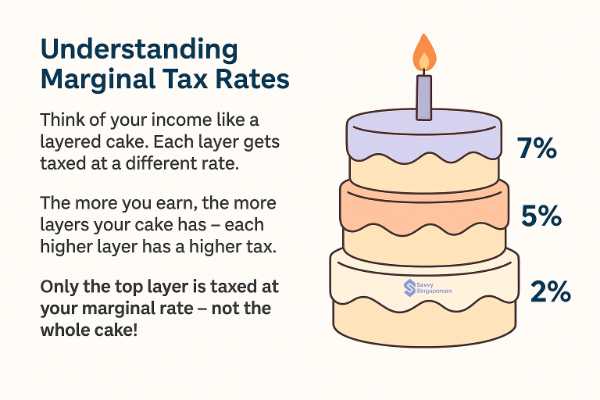

Think of Singapore’s income tax as a tiered cake – the higher the layer of income, the higher the tax rate on that layer. By contributing to SRS, you’re basically removing the top layer of that cake (up to S$15,300 worth) from the tax man’s plate. The result? That top slice of your income isn’t eaten by taxes now. How much tax you save on it depends on how “rich” that slice is in tax – which is where your income level and marginal tax rate come in.

Marginal tax rate, explained: Singapore uses a progressive tax system with brackets. Your marginal tax rate is simply the tax rate on your next dollar of income – essentially, the rate of the highest bracket your income reaches. For example, if part of your income falls in the 7% tax bracket, your marginal rate is 7%. If your income is high enough that your top portion is taxed at 18%, then 18% is your marginal rate. It’s the rate applied to the last dollar you earned.

When you contribute to SRS, you’re deducting from that last (highest-taxed) portion of your income first. So, the tax saved is roughly “your marginal tax rate × S$15,300”. A high marginal rate means each dollar of SRS contribution saves more tax. A low marginal rate (or no tax at all) means the SRS contribution yields little to no tax savings. Let’s see this in action with actual numbers.

Singapore’s Progressive Tax Rates (YA 2025) in Brief

Before looking at examples, it’s good to know the playing field. Singapore’s resident income tax rates for YA 2025 are progressive – the first S$20k of chargeable income is taxed at 0%, the next portions at 2%, 3.5%, 7%, and so on, with higher percentages for higher income portions. The highest tax rate for individuals in YA 2025 is 24% for income above S$1 million (for context, the rate was capped at 22% before, but new top tiers of 23% and 24% now apply to ultra-high incomes). Most working professionals will fall in lower brackets. Here’s a quick summary of the key brackets for YA 2025:

| Income Band (Chargeable Income) | Tax Rate Applied to That Band |

| First S$20,000 | 0% |

| Next S$10,000 (S$20,001 – S$30,000) | 2% |

| Next S$10,000 (S$30,001 – S$40,000) | 3.5% |

| Next S$40,000 (S$40,001 – S$80,000) | 7% |

| Next S$40,000 (S$80,001 – S$120,000) | 11.5% |

| Next S$40,000 (S$120,001 – S$160,000) | 15% |

| Next S$40,000 (S$160,001 – S$200,000) | 18% |

| Next S$40,000 (S$200,001 – S$240,000) | 19% |

| Next S$40,000 (S$240,001 – S$280,000) | 19.5% |

| Next S$40,000 (S$280,001 – S$320,000) | 20% |

| Next S$180,000 (S$320,001 – S$500,000) | 22% |

| Next S$500,000 (S$500,001 – S$1,000,000) | 23% |

| Amount above S$1,000,000 | 24% |

In short, as your income crosses each bracket threshold, the extra income in the new bracket is taxed at a higher rate, but the earlier income is still taxed at the lower rates. (So a person making S$60k doesn’t pay 7% on the entire 60k – only the portion above $40k is at 7%, etc.)

Now, with these rates in mind, we can calculate how much tax is saved by using the full S$15,300 SRS relief at different income levels.

Tax Savings from Maxing SRS: Examples at Different Incomes

Using the YA 2025 rates, here’s a table of annual income vs. estimated tax saved when contributing the maximum S$15,300 to SRS (assuming no other reliefs for simplicity). This shows why SRS is a bigger boon for higher incomes and minimal for lower incomes:

| Annual Income (S$) | Approx. Tax Saved with SRS (S$) |

| 30,000 | 200 |

| 60,000 | 1,071 |

| 100,000 | 1,760 |

| 160,000 | 2,295 |

| 200,000 | 2,754 |

| 500,000 | 3,366 |

(Calculations based on Singapore’s resident tax brackets for YA 2025. “Tax saved” is the difference in tax payable before vs after a S$15,300 SRS relief.)

You can see the trend: the higher the income, the more tax you save by maxing out SRS. A middle-income person earning S$60k saves around S$1.07k, while someone earning S$200k saves about S$2.75k, and a very high earner at S$500k saves roughly S$3.37k in that year. Meanwhile, someone at S$30k income only saves about S$200, and if your annual income is S$20k or below, you’d save $0 because you weren’t going to pay any tax anyway!

Why do these savings climb with income? It’s all about the marginal tax rate of that S$15,300 slice:

- At S$30k income, your top tax bracket is just 2%. SRS only spares income that would’ve been taxed at 2%, saving ~S$200 (which is 2% of 15.3k). If income were a ladder, you’re only on the first couple of rungs – taking away a rung doesn’t change much.

- By S$60k, your top dollars are taxed at 7%. SRS removes those 7%-taxed dollars (up to 15.3k worth), saving about S$1,071 (roughly 7% of 15.3k).

- At S$100k, you’re in the 11.5% bracket. Now each SRS dollar avoids an 11.5% tax, netting ~S$1.76k saved (11.5% of 15.3k).

- At S$160k, top bracket 15% → save ~$2.3k (15% of 15.3k).

- At S$200k, top bracket 18% → save ~$2.75k (18% of 15.3k).

- At S$500k, top bracket 22% → save ~$3.37k (22% of 15.3k).

In essence, the SRS relief is most effective on the highest taxed portion of your income. The more of your income that sits in those high tax brackets, the more tax dollars SRS can save you by shielding S$15,300 of that portion.

Why Low Earners Save Little (or Nothing) and High Earners Save More

If you’re a low-income earner, you might notice SRS doesn’t give much of a “reward” in tax savings. That’s because Singapore’s tax system already spares low incomes – remember, the first $20k is not taxed at all, and even up to $30k the tax is very low. If you earn say $25k, you pay only about $100+ in tax normally. Using SRS to cut your taxable income might reduce your tax bill from ~$100 to $0 – saving you a hundred bucks. In fact, if your income is below ~$22k, you likely pay $0 tax without SRS, so contributing to SRS wouldn’t save any tax (you can’t go below $0 tax). It’s like having a discount coupon when buying something cheap – a $50 voucher doesn’t matter if you’re only spending $20 in the first place.

On the other hand, high-income earners benefit a lot more because they are in the higher tax brackets. If you’re making six figures, the top slice of your income is taxed at rates like 15%, 18%, 19% etc. Using SRS is akin to using a hefty coupon on an expensive purchase – that $15,300 relief is applied to income that would’ve been taxed quite heavily. For example, at $200k income (18% top bracket), an SRS contribution saves you about $2.7k of tax. At $500k (22% bracket), it’s over $3.3k saved. This is real money back in your pocket (or rather, left in your SRS account, growing tax-free) just for shifting some income to retirement. In short, the higher your income (and tax rate), the more worthwhile SRS becomes as a tax-saving tool. High earners essentially get a ~20%+ “rebate” on that $15k contribution via tax savings, whereas low earners might only get 0–5%.

Another way to view it: Singapore’s tax system is progressive, so SRS offers progressive relief. It doesn’t do much if you weren’t going to owe much tax, but it meaningfully cuts the tax for those who owe a lot. That’s also why the government encourages things like SRS – it incentivizes higher earners to save for retirement by giving them a tax break for doing so.

Where Does the Tax Benefit Plateau (and Why)?

You might be thinking: if higher income means more tax saved, does that mean billionaires save a fortune with SRS? Not exactly – there’s a cap to the benefit. Since you can only contribute up to S$15,300 each year (for locals), that’s the maximum income amount you can shield from tax annually. So there is an upper limit to the dollars saved.

Imagine someone astronomically wealthy – even if their marginal tax rate is the top 24%, applying that to $15,300 gives a tax saving of about $3,672 for the year. That’s basically the ceiling (and it’s relatively small compared to their huge income). In our table, you can see by $500k income, the tax saving (≈$3.3k) is already close to this max. For incomes beyond that, it only inches up a bit more. For example, at a $1 million income (23% marginal rate at that level), the saving is about $3.5k; at $2 million (24% rate), around $3.67k. It plateaus because no matter how much higher your income goes, you’re still only getting tax relief on $15,300 of it each year, and that relief can’t exceed ~24% of $15,300.

So, whether you earn $500k, $5 million, or $50 million, the absolute tax dollars saved per year from SRS doesn’t increase beyond that range of a few thousand dollars. This is an important point: SRS is great for what it is, but it won’t drastically shrink a super high earner’s tax bill – it just shaves off a fixed chunk. In percentage terms, the benefit actually matters most to middle/high-middle income folks (for whom $2k–$3k less tax is significant). For ultra-high earners, $3k is a drop in the bucket (but hey, every bit counts). And for very low earners, SRS might not be beneficial at all, since they may be under the taxable threshold or already paying very little tax.

Tax relief cap: Additionally, note that the government imposes an overall personal income tax relief cap of $80,000per year. This means if you have a lot of other tax reliefs (from things like CPF cash top-ups, donations, family-related reliefs, etc., plus SRS), the total relief you can claim is limited to $80k. Practically, $15.3k of SRS by itself won’t hit that cap, but if you’re a high earner already claiming tons of reliefs (for example, wealthy individuals with large families and reliefs), you can’t reduce your assessable income beyond a certain point. SRS is included in that $80k cap. It’s worth keeping in mind, though most ordinary taxpayers won’t have reliefs anywhere near $80k. The key message is: you can’t zero out your taxes completely through reliefs – there’s a limit to how much you can slash off your taxable income in total.

Don’t Forget: Future Withdrawals are Partially Taxable

Before you rush to put money into SRS purely for the tax break, remember that SRS is not tax-free forever. It’s more of a tax deferral and reduction strategy. Your contributions and investment gains in the SRS account grow without being taxed yearly (unlike if you earned interest or dividends outside, which might be taxable; SRS investment returns are tax-free while in the account). However, when you finally withdraw from SRS (which typically you’d do after the statutory retirement age), only 50% of the withdrawal amount is taxable.

Why only half? It’s a special concession to encourage participation – effectively you got a tax break going in, and you get another break coming out by only being taxed on half the money. In many cases, by retirement your income is lower, so those withdrawals might even be taxed in lower brackets (or sometimes not at all, if kept small). For example, if you withdraw $40k from SRS in a year, only $20k is counted as taxable income – which might end up tax-free or minimally taxed depending on other income. This is a pretty favorable treatment, but it’s important to plan: early withdrawals (before retirement age) trigger penalties and are 100% taxable, so SRS is truly for long-term needs.

In simple terms, SRS gives you tax relief now in exchange for locking the money for retirement (and even then taxing only half of it later). It’s a trade-off: immediate tax savings and investment growth versus liquidity. So, make sure you won’t need this chunk of money until retirement.

Summary & Should You Consider SRS?

To wrap up, SRS contributions can indeed save you tax, but how much depends on your income and tax bracket. For low earners, the savings are minimal (and might not justify locking up the funds). For middle to higher earners, maxing out SRS can shave a notable amount off your tax bill – often in the range of a thousand to a few thousand dollars each year. There’s a cap to the benefit (you won’t save more than roughly $3.6k a year even at the highest incomes, due to the contribution limit and tax rate ceiling), but the scheme also offers the advantage of tax-deferred investment growth and only half-taxed withdrawals in the future.

SRS is a helpful tool in your tax planning toolkit, especially if you are in a higher tax bracket and have spare funds that you can commit to retirement. It’s like getting a yearly tax “discount” for saving for your future. However, always evaluate your own situation – consider your cash flow needs, other reliefs, and retirement goals. As IRAS itself advises, “please evaluate whether you would benefit from tax relief on your SRS contributions, and make an informed decision”. If you’re comfortable locking away money till retirement and you’d otherwise be paying significant taxes now, SRS could be a good fit to reduce your tax burden while bolstering your retirement savings.

In the end, it’s about balancing tax savings with financial flexibility. If that balance makes sense for you, contributing to SRS is a win-win: you save on taxes today and save for your golden years. Happy planning, and may your tax savings work towards your future goals!